This post was written by Portland lawyer Cynthia Newton. She previously shared her concerns about commercial truck operators. Today’s post is about the insurance gap faced by bicycle users. It’s an issue we’ve covered previously here on BikePortland, but it’s so important we felt it was worth re-upping.

This is one of those things that’s not pleasant to think about, but important to know.

Bicycle riders and walkers who are involved in a collision with the driver of a motor vehicle often suffer serious injuries, requiring emergency medical care, surgery, hospitalization and short or long-term disability. Many Oregon drivers carry the minimal automobile insurance limits of $25,000. Serious injuries combined with this minimal amount of coverage combine to create a gap between the funds needed to pay medical expenses and to be fully compensated for lost income and non-economic damages. Put more simply: The injured’s damages exceed the at-fault driver’s insurance coverage.

As lawyers who work with bicycle riders, we see the consequences of this situation far too often.

The victim’s own automobile insurance Personal Injury Protection (“PIP”) coverage and Underinsured Motorist (“UIM”) coverage play a key role in providing financial relief and compensation. Here’s why PIP and UIM coverage are so important to Oregon’s vulnerable road users and why buying more of each may be worth the extra pennies:

Take, for example, Joe, one of our seriously injured clients who was commuting by bicycle in a bicycle lane when a minivan driver, suddenly and without warning, turned right directly in front of him — a the classic “right hook.” In the resulting collision, Joe broke his foot and leg. An ambulance took him to the emergency room where doctors took x-rays and fitted him in a cast. Several days later his orthopedic surgeon placed pins in his foot to hold the bones in place. After five months of painful physical therapy his surgeon recommended another surgery to remove the pins which were impeding mobility. He was disabled and unable to work for 12 weeks immediately after the collision and for another month after the second surgery.

Joe’s medical bills were $85,899.33. His income loss $20,000. His non-economic damages for pain and suffering, loss of enjoyment of life and permanent limitations, are at least $100,000. The driver who struck Joe had Oregon minimal liability coverage limits of $25,000/$50,000 creating the obvious problem: With over $100,000 in economic losses and even greater non-economic losses, using these funds alone, Joe will not be adequately compensated by the at-fault driver’s $25,000 in liability coverage.

Here’s a crash course on how auto insurance coverage works in Oregon…

Personal Injury Protection (PIP)

In Oregon, medical bills to care for a bicycle rider’s injuries caused by a collision with a motor vehicle operator are paid by insurers in this order: 1) the bicycle rider’s own automobile insurance Personal Injury Protection (“PIP”) coverage, if any; 2) the rider’s health insurance, if any; and 3) the driver’s automobile insurance under the policy’s PIP coverage.

Under-insured Motorist Coverage (UIM)

Oregon auto policies also include UIM. UIM coverage is designed to compensate the vulnerable road user for damages suffered for which the at-fault vehicle operator is responsible, yet not insured.

Minimal PIP and UIM Coverage Requirements

Insurers writing Oregon policies are required to write $15,000 of PIP medical coverage and 70% of lost income for up to one year (under certain circumstances) and $25,000/$50,000 per person/per collision of UIM coverage.

How PIP and UIM Compensate

Joe had $15,000 in PIP which was paid to the hospital for emergency and in-hospital care. His health insurance paid next — about $40,000 of the remaining $70,000. The driver’s insurance paid nearly $10,000 of its $15,000 PIP limits for Joe’s co-pays, deductibles and out-of-pocket expenses. After all three insurers’ payments, Joe has medical expense balances of $15,000. Joe’s PIP also paid him 70% of his lost income during the period when he was off work, paying 70% of his $20,000 lost income.

Any additional compensation, for past and future income loss or earning capacity, pain and suffering and permanent impairment, had to come from the driver’s liability coverage of $25,000 and Joe’s own UIM coverage, also $25,000. The total recovery was $50,000. (Seeking money damages from the at-fault driver was impractical in light of the driver’s financial situation and assets.)

Advertisement

Considering nearly $100,000 in medical expenses, $20,000 in lost income, months of pain, suffering and loss of enjoyment of life, and permanent impairment, Joe’s case could reasonably be valued at $250,000. Instead, he can recover only $25,000 from the mini-van driver. The at-fault driver maintained insurance to cover just 10% of the damage he inflicted.

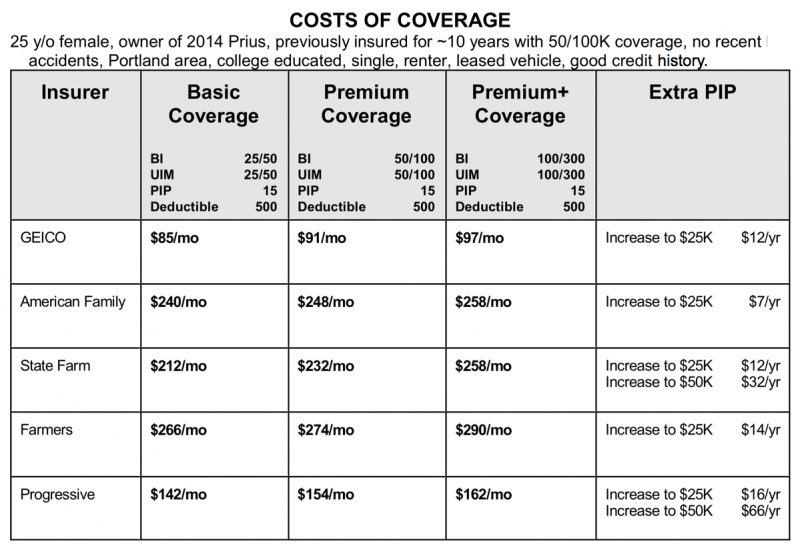

Bicycle riders wishing to guard against this risk of being under-compensated after an injury-causing collision can increase their policy’s PIP and UIM coverage limits. Our informal research shows that increasing these limits can cost relatively little in light of the considerable benefits they provide when a rider, vulnerable to the effects of a collision with a motor vehicle operator, is injured. We asked five auto insurers what it would cost for a 25-year-old female Portlander who owns a Prius and had been insured for 10 years with good credit and no history of collisions, to increase her PIP and UIM coverage.

This table summarizes our findings:

The table shows that this bicycle user can increase her PIP from $15,000 to $25,000 for between $12.00 and $16.00 per year. She can increase her PIP to $50,000 for between $32.00 and $66.00 per year.

One advantage to having more PIP coverage available to pay medical bills is that while many health insurers control the providers its insureds can see for treatment, PIP has no such restrictions. Also, PIP has no co-pays or deductibles and the medical provider is required to accept payments set by statute and write off the balance.

That same policyholder can increase her UIM coverage from the basic $25,000 to $50,000 for between $6.00 and $20.00 per month and to $100,000 for between $12.00 and $46.00 per month. Additional UIM coverage is then available to compensate the rider more fully for unpaid medical expenses, lost income and non-economic losses. Since legislation effective January 1, 2016, UIM coverage “stacks” or sits on top of the driver’s liability coverage. (For more about HB 411 see coverage on BikePortland.)

Insurers aren’t required to tell their customers about the availability of higher PIP and UIM limits. And, at these prices they may have little incentive to do so.

Unfortunately, in many cases, whether someone injured biking or walking will or will not be compensated fully will depend on his or her own automobile coverage. While this may be unfair, until legislation is passed requiring higher automobile user liability limits, drivers won’t have enough coverage to compensate those they seriously injured. According to one 2015 study, 12.7 percent of Oregon drivers were uninsured. Many more, we find, are under-insured.

Until the legislature takes action to help protect bicycle users from uninsured — and under-insured — drivers, Oregon’s vulnerable road users should consider whether they can pay a bit more to secure higher PIP and UIM limits to provide themselves some measure of self-protection.

— Cynthia Newton is a partner in the law firm of Thomas, Coon, Newton & Frost. TCN&F is also a BikePortland sponsor.

Never miss a story. Sign-up for the daily BP Headlines email.

BikePortland needs your support.

Thanks for reading.

BikePortland has served this community with independent community journalism since 2005. We rely on subscriptions from readers like you to survive. Your financial support is vital in keeping this valuable resource alive and well.

Please subscribe today to strengthen and expand our work.

When were these PIP & UIM limits instated? Do they have a schedule for increasing or does this have to happen at the legislature’s initiative?

I disagree with the idea that people who bike or walk for transportation should 1) pay car insurance and/or 2) pay more for car insurance. I would much rather purchase disability insurance than an insurance product that profits from carnage and global environmental tragedy.

PS: I have the absolute minimum car insurance possible at metromile and am considering getting rid of my coverage entirely.

These are serious questions for people who are truly car-free.

I’ll bet buying up the PIP and UIM on your own policy is relatively inexpensive.

On my policy, it’s $7/month to raise my UIM from 25,000 per person/50,000 per incident to 1,000,000 per person/1,000,000 per incident. However, it also requires me to up my Bodily Injury Liability to the same amount, which covers anyone I hurt in an ‘auto accident’. And that costs an extra $18/month.

disability coverage is cheaper (albeit through my work).

It isn’t fair, but this is a reality. This is the cold-hard evidence of the externalized automobile costs that we talk about here. Minimums should be in the $500,000 – $1,000,000 territory if we really want to work to eliminate the accident/injury externalities.

I’d start with seizing cars from uninsured drivers and upping the penalty for hit and runs. Right now there’s probably only an 80% chance that you’ll even have a driver’s insurance company to go after in the first place.

What if I don’t have auto insurance?

This article from bikeportland is relevant to your question, the answer is not awesome though: https://bikeportland.org/2010/01/05/editorial-the-bicycle-insurance-gap-and-what-we-can-do-about-it-27777

I think carrying additional insurance is a very good idea. I have increased my bodily injury and property damage liability insurance to 500k along additional PIP and 500k for uninsured/underinsured motorists per occurance. This allowed me to also add an additional million dollar umbrella policy that covers motor vehicle injuries along with other things. The umbrella is a few hundred a year, and the increase to my max coverages were really not that much. This is the kind of level of insurance that we should be requiring all drivers to carry, not just cyclists who are afraid of being hit. It is unfair to require people to carry large amounts of extra insurance to cover people who are underinsured but that is the system at the moment. I am fairly certain that the minimum coverage levels now are the same as they were when I was hit by a motorist in 1990.

It’s worth noting that your under/uninsured coverage only kicks in if the other insurance company admits liability and doesn’t cover the rest of your costs after your PIP and medical insurance. If they don’t admit liability (and that never happens with car vs bicycle crashes, right?) the PIP is the first thing to be drawn from, and I can tell you from experience that it’s easy to spend the entire $25,000 in your first 10 minutes in the trauma center.

Is it impossible for those of us who do not own a car to buy PIP coverage?

Can you carry auto insurance if you don’t have an auto?

My wife and I have an auto policy and an umbrella policy. When we were considering going car-free, I asked my insurance agent about the implications. I was told that I would need a named non-owner policy to replace the liability coverage in our auto policy. Unfortunately the named non-owner policy was nearly as expensive as the auto policy. This was a few years ago, so things may have changed. In any case, searching for “non-owner policy” is a reasonable place to start.

disability coverage would protect against the income loss mentioned in this piece and is often more affordable than an auto insurance policy (or increased coverage in an auto-insurance policy). assuming someone has OK health insurance then this option should have been mentioned by the author.

My partner’s agent offered such a policy, but added that it’s a much better deal to insure a car with with scrap value than no car at all.

YMMV.

Ugh. It’s amazing how our society is structured to assume that everyone drives. We have a long way to go.

“[…] it’s a much better deal to insure a car with with scrap value than no car at all.”

Wow. Okay, that’s what I assumed but surprising all the same to actually hear it confirmed. A scrap title (and car) can be had for as cheap as $125. So… that may be the initial upfront cost to gain access to the PIP insurance ride!

“Joe’s medical bills were $85,899.33” – This figure sounds right, but health insurance companies negotiate this down to around $20K….that’s one of the big benefits of insurance…the “insured rate”. If you didn’t have health insurance, you would pay the $86K. And then his annual out of pocket should be capped at around $8k. My wife just had the same injury happen to her.

This is where I’m at. No car, no auto insurance; however, I do have medical coverage with a $3,500/year maximum out of pocket. I hit that limit every year without fail. So the idea of having to pay my own medical bills due to someone else’s negligence doesn’t terrify me financially much.

Should I seek PIP coverage given my relatively low maximum out of pocket medical insurance? I’d hate to insure a car chassis that just sits in my driveway or whatever it takes to gain access to PIP for an auto policy I would otherwise never use. Note, I don’t have said car chassis, I’m simply using it as an example of an extreme hypothetical.

Maybe find the smallest scooter or motorcycle you can license and buy insurance for that. Buy an old cheap one that doesn’t work, otherwise you might be tempted to ride it. 🙂 Probably have to get a motorcycle license to license it though.

“I’d hate to insure a car chassis that just sits in my driveway…”

No prob. Just park it in the street!

look into disability insurance. often this provides significant coverage for relatively low cost.

I’m sure there is an insurance policy of some type even if you don’t own a car.

Cynthia, what do you think – is this policy adequate?

Under liability I have bodily injury 250K/500K, property damage 250K (in case you hit a Lamborghini).

Under PIP it says Medical 25,000 and Income loss 3000/month.

Under UIM it says bodily injury 250K/500K.

I have BIPD liability (Cynthia, what’s that?)

I have emergency road service (towing), car rental, use of non-owned cars, etc.

This is State Farm and the premium is less than $65/month. I do have several other policies so I get multi-policy discount, have never had an accident or a claim (other than dinged windshield and towing), and my car is old and only worth about $1,500, and I’ve been with them for decades. Also, I have taken driver safety courses thru work in years past.

Is it true that Car2Go or Reach Now membership might cover you as a cyclist in a crash? I’ve heard it’s true from someone who had a settlement but it’s hard to believe. I’ll need to get in touch with those companies, but curious if anyone knows the answer.

The injustice of the insurance math really stings, but this was super helpful info. Thank you, Cynthia.

This is quite an indictment of health care costs.

Considering that the majority of the settlement example listed above was for lost wages and pain/suffering, I’m not sure how you draw that conclusion. It sounds like his injuries were significant.

The big take-away from this story is that automobile use imparts huge externalized societal costs, in the form of lost wages and pain/suffering. The vehicle operators rarely pay these costs directly, and thus have little incentive to operate more safely.

My Canadian BF was astounded at the low insurance options available to drivers in the US. His point was that he wanted way better insurance here than Canada, since in Canada every one is covered by health insurance, whereas here an accident which requires medical care for someone without insurance would be way over your limit. I always opted for low coverage thinking that I didn’t drive much, but have come around to his way of thinking. This article only further supports that theory.

Especially when close to 1 in 10 drivers are not insured at all, most drivers are not insured enough to do you any good if something major happens, and many drivers will flee the scene if they hit you anyway. You absolutely cannot count on outside insurance if you get hit.

My family has a $5million umbrella policy that will kick in after all other policies have been maxed out, I would hate it if my negligence resulted in injury that could not be compensated by insurance (also we have a house and retirement savings we need to protect).

Based on the premium table above, it looks like the 25 y.o. female is being taken to the cleaners. I’m a 61 y.o. male, and my 6 MONTH premium for full coverage, and 250K/500K bodily injury liability, 250K property damage, PIP medical 25K + 3,000/month income loss, $100 deductible comprehensive, $250 deductible collision, towing, car rental, UIM bodily injury 250K/500K, use of non-owned cars, BIPD liability, costs less than $65/month. My car is only worth $1500 which helps. I do get good driver discount and multi-policy discount, no claims for decades, etc.

You’re 61 . . . statistically a safer driver than a 25 year old, I would guess.

Yep; it’s all based on statistics. I have talked to young people, with good driving records, who pay the same amount for their insurance for four months, as I (at age 70), do for a full year.

The insurance gap for anyone who isn’t covered as a driver is pretty appalling. Wish we had some kind of bike transportation advocacy group to push a bill requiring any company insuring cars in Oregon to offer a policy covering car crash participants who are not car owners and are not car passengers at the time of the incident.

Since pedestrians don’t have much kinetic energy and bike riders hardly ever kill people it could be pretty cheap, compared to car coverage. The premium could be 70% overhead and nobody would know the difference.

Our insurance mandate is incredibly out of whack. It’s insane that people can own a car, operate it on the road and carry either very low insurance or none at all. Worse yet, responsible people who choose to go car-free are really put in a hard place, since there is no reasonable way to get insurance that covers the gap created by this broken system.

Sadly, there are zero prospects for legislative fixes. Find me the legislator who can relate to not owning a car or who would place the value of fixing this broken system for the car-free and car-light (included because there are ways to have intermittent insurance for those rare times one chooses to drive without having on-going coverage). Such a legislator would be a unicorn indeed. And yet one would have no difficulty at all finding legislators (or a governor) who will go on and on about how we must deal with climate change (as long as it doesn’t involve reducing driving, the number one source of emissions from Oregon).

If we ever get a government owned/funded/operated single payer medical plan, I guarantee this legislative gap will be plugged. When the government ends up bearing responsibility for treating injuries caused by the negligence of others, they make sure that those causing the damage have insurance to cover it.

B. Carfree,

Found that unicorn you wanted:

http://www.thinkgeek.com/product/e5a7/

🙂

Not an insurance expert at all, but if you have health insurance, aren’t you then covered for the bulk of medical bills in the effect of a serious injury? I realize that there would be a deductible, copays, potentially $5-10K out of pocket. Which would be bad but better than no coverage.

Or are you finding that the limitations of most health insurance coverage are big enough that injured cyclists are seeing more than $5-10K out of pocket?

Of course, health insurance won’t pay for lost wages, disability, pain and suffering, new bike, and all the other sorts of damages.

You’re forgetting about the part where they hire Xerox to come after you for any proceeds you acquire after they’ve paid the bills. As anecdotal evidence, I had auto insurance, a $15k pip and medical insurance when a car entered my path and drove me to the pavement. In all, after the insurance payments, I was over $18,000 out of pocket.

This is not a little deal, and insurance doesn’t protect you- they only protect themselves.

My question is why the victim’s health insurance should pay to repair the damage inflicted by a motorist – the motorist who is at fault should bear the cost and responsibility for making the victim whole.

They work this out later. Note that Joe’s $86K bills were for a broken foot and leg. This is relatively lucky for a collision with a multiton chunk of steel. Just so happens a buddy and I got taken out by a car a few years ago — he had $180K in costs.

About a year later, his health insurance had me make affidavit to help them with their process of recovering damages.

No matter what the case, you need coverage both to protect yourself from others and to protect others from your mistakes whether or not you ever get in a car. A million garden variety accidents such as slipping on a wet floor or stairs where you live can cause life changing injuries.

A lot of people don’t have assets that can cover your losses and even if you don’t care about trying to do right by people you hurt, you risk your assets and wages.

Thanks for a very informative post. I’m surprised the writer didn’t mention subrogation, which allows health insurers to collect victims’ liability/UIM settlements. In many cases where cyclists/pedestrians require hospitalization, victims will not receive any compensation – not even to cover out-of-pocket medical expenses. We need a Make Whole law in Oregon like the one Colorado passed in 2010! (Info on the CO law can be found here: https://www.coloradolaw.net/news/make-whole-bill/ )

I take it the rider didn’t have short or long term disability insurance through work?

I recently suffered a pretty serious injury in a scooter (motorcycle) crash, not involving another party. I quickly found my PIP doesn’t apply to motorcycles (and as it’s not required to by statute, generally that will be the case unless specific coverage is purchased). Would the same be true for a bicycle crash without an auto involved?

I crashed my bicycle in August 2016 and broke my arm. I have comprehensive auto insurance with Travelers but it did not cover my crash as there was no motor vehicle involved. I had to use my medical insurance to pay (a Bronze plan from the health insurance exchange), which meant I was out of pocket for the $7,500 deductible (medical bills were around $50,000), and lost pay while I couldn’t work (I got back to work as soon as I could, p/t within a week, f/t after about ten days).

I grew up in Australia and got my first driver’s license there. In Australia, every motor vehicle that is registered to be driven on public roads must carry a Compulsory Third Party liability insurance (in New South Wales they refer to it as CTP Green Slip). This policy provides for AUD 20 million in coverage to pay for injuries sustained by third parties (everyone but the at-fault driver). In New Zealand, where I also lived for a while and got my second driver’s license, the country abolished all personal injury lawsuits decades ago and set up the Accident Compensation Commission, which compensates all victims of injuries – however, NZ is much more ready to prosecute and punish those who cause injuries than we are in Oregon (so is Australia btw).

I find it absolutely appalling that the victims of traffic violence are left to fend for themselves. It is one thing if a road user has a single vehicle crash (like I did a couple of years ago on my bike) and is injured, then he/she is responsible. However, when a motorist causes injury, we only require them to have a token amount of insurance ($25K buys almost nothing in emergency medicine these days) and rarely are they prosecuted or punished in any meaningful way – in fact our public prosecutors seem to go out of their way to exonerate motorists.

We really need to change this situation, and approaches like those taken in Australia and New Zealand, while not perfect, at least offer the innocent some chance of recovery.

writing articles for a blog? You need to drop the haughty attitude and stop telling me what to do.

It’s your funeral, after all.

Why be prepared? You can always have your family start a Go Fund Me to keep you on life support later.

telling other people how to behave is just as distasteful in a comment on a blog post telling you to buy insurance as it is coming from the window of a truck telling you to get off the road. (and you don’t know me, my level of coverage, my family situation, or my DNR status, but keep being snarky on the internet if it makes you feel better)

Telling the owner of a blog you don’t support what to do is distasteful too, by that measure.

I don’t know about you, but I have a bad taste in my mouth now.

This exact thing happened to my father-in-law. He was struck by a trailer that was not properly attached to a pickup in Cottage Grove while walking down the sidewalk. The driver had $50k in liability insurance which did not even cover 1/2 of the cost of his initial surgeries. He ultimately died from these injuries after several very difficult months for our family where he was in hospitals and care facilities. He wasn’t wealthy, and the estate matters are a complicated mess with the various hospitals and care facilities try to recover what little they can. That said, the OR legislature needs to increase driver’s insurance limits. I drive a car, and I buy extra insurance on my vehicles. Cars and trucks cause the vast majority of medical expenses, and those costs should not be “externalized” to vulnerable road users. All of that said, this article has good advice. I’m an avid cyclist as well. Given the potential gap and related impacts it can have, I’ll buy this this insurance.

Good information for folks to know, but also important to mention (especially as a lawyer) that those injured in these types of accidents can hire a personal injury attorney to recoup all costs plus compensation for pain and suffering. These attorneys aren’t paid until you get a settlement – ie no costs up-front.

I was hit in a right-hook requiring two surgeries over six months, had PIP through my partner’s auto policy, also had health insurance, AND hired an attorney. In the end, all of my costs were covered and I walked away with the equivalent of a year’s worth of salary for my trouble.

The PIP helped cover any out of pocket costs (copays or deductibles) that I faced early on, but ultimately the PIP coverage was repaid by the settlement, as was my health insurance. Everyone wins except the driver/their insurance!

PIP insurance is not going to compensate for pain, suffering, lost wages – etc. I’d never been involved in any legal proceedings before this, but I wouldn’t hesitate to go this route if ever hit again.

“Seeking money damages from the at-fault driver was impractical in light of the driver’s financial situation and assets.”

You can’t squeeze blood from a stone. So where did the lawyer get the settlement money from? Everyone paid their required part and there’s no money left.

Your situation was preferable. The whole article is about a situation different from yours–when you’re hit by someone who is underinsured and doesn’t have financial resources to compensate you (often substantial overlap in those categories). For those situations, the author recommends you carry insurance to protect yourself.

Your situation was different from that described in the original blog post in that the driver who struck you either had assets or insurance to compensate you for the injuries inflicted. My biggest problem is that in the USA in general, and Oregon in particular, motorists are not required to have very much insurance. It would be preferable if we required proof of adequate insurance when we register an automobile, and rigorously enforced registration laws (i.e. immediately impound unregistered vehicles found on public streets, and if they’re being driven, cite the driver). We also need to update what we consider to be adequate insurance, in my view the minimum would need to be of the order of $5 million, which we might need if a motorist ran a tour bus off the road and injured 50 passengers.

I don’t understand why Bodily Injury Liability (which has much higher limits) doesn’t figure into example Joe. This definition from Liberty Mutual…

“When you are found legally responsible for a car accident, bodily injury liability coverage is the part of your insurance policy that pays for the costs associated with injuries to the other person or people involved. This coverage also provides a legal defense in the event that you are sued for damages.”

So if the minivan driver is found at fault, wouldn’t his policy have to pay out of BI coverage? I note that it’s on the chart above, too.

The minimum required in Oregon is $25,000, which barely covers a trip to the ER. The minivan driver likely had the bare minimum.

I just added $50,000 in additional PIP coverage to my USAA – it only costs $4/month extra.

I live car-free. I have not owned a car in over 25 years. I do not plan to own a car ever again. If I am struck by a car while walking, I should not have to carry auto insurance in order to be covered. Pedestrians don’t generally kill people when they collide with them. Nor do they tend to cause injury to the one they bumped into, because no pedestrian weighs 2,000 pounds or travels at freeway speeds.

This is why I don’t (and shouldn’t) need an operating license or insurance in order to walk in Oregon, or any other state.

The notion that I would have to buy a scrap car, in order to buy car insurance, in order to then buy more PIP coverage, is a tasteless joke at my expense and the expense of everyone else who does not own or drive a car. All it does is provide another revenue stream for the insurance industry.

No thank you. I do not exist in order to keep the insurance industry afloat.

Welcome to America.

If medical care were free at the point of delivery the way it is in civilized countries, individuals would not need 7 or 8 exotic insurance instruments to insure, or reinsure every facet of their life.

I have been sued and sued another party. Afterwards my limits went to 250/500. Anyone who carries the minimum and has read this is stupid. 250/500 should be compulsory.

i only drive a few hundred miles a year and have almost all my net worth in protected retirement accounts so i don’t care if someone sues me. the fact that i have to pay close to the same amount for car insurance as someone who drives 5,000 miles is utterly ridiculous. in fact, almost all the fixed costs of driving are designed to be punitive towards people who drive less (licensing, registration, insurance).

A judgement is a judgement. Plus, what kind of human are you if you maim or kill another and refuse to pay?

insurance should reflect relative risk. my relative risk is asymptotically close to zero.

What about cyclists or walkers that don’t have a car, and/or can’t drive?

I found that I couldn’t get insurance to give me any PIP/UIM protection while I lived in Oregon because I didn’t own a car.

With a little injenuity, it’s easy to “own” a car that never parks in your driveway or never touches a street. If you can logon to this website, you can figure it out.

car head.

I wanted to take a minute to respond to a few questions/comments that emerged here:

1. Why should bike riders and pedestrians have to buy insurance instead of motorists being required to have insurance or have higher limits?

Oregon currently requires drivers to carry bodily injury liability limits of $25,000 per person/$50,000 per collision. I agree that these are too low and laws should be passed requiring higher limits. My goal here was to inform BP readers of how much insurance drivers have to carry and to suggest, to those who own insured cars and also ride bikes, that they could consider raising their PIP and UIM limits as a measure of self-protection against an underinsured or uninsured motorist.

2. What limits should a prudent bike rider or pedestrian have?

Several of you asked this. I think carrying Oregon’s required $15,000 PIP and $25,000/$50,000 underinsured motorist coverage is far less than ideal, especially when buying more is relatively inexpensive.

The two next levels of PIP coverage are usually $25,000 or $50,000. $25,000 is nice and will cover most ER visits we see after bike crashes.

For underinsured motorist coverage, $50,000 does not go much further than $25,000.

$100,000 provides considerably more protection and is a coverage level that would make an appreciable difference in many claims.

3. Are you saying buy a car or motorcycle to get PIP or UIM?

I am not saying this. In fact, there were several companies considering selling insurance to those who ride a bike and don’t own a car, but these did not come to fruition. Also, it is important to know that if you buy a motorcycle or scooter to get PIP coverage, insurance sales folks do not have to include PIP unless you ask for it specifically. I’ve seen many a motorcyclists very surprised to learn that she did not have PIP coverage she thought she had.

4. Why not buy disability insurance instead?

This certainly is a possibility, but I would caution that disability carriers have very specific requirements which must be met before they pay benefits.

5. Medical costs, health insurance and subrogation

We all know medical costs are skyrocketing and health insurance only covers part of them. And yes, health insurance companies almost always have subrogation clauses in their policies, requiring that an injured insured repay them if that insured makes a recovery from a liability insurer. This process is nuanced and there are several ways an attorney familiar with these coverages and how they impact bike riders can aid an injured cyclist or pedestrian in obtaining a recovery even in the face of large medical expenses and health insurer subrogation.

Cynthia, Thanks for the post! These are things we don’t think about, don’t know about, and don’t want to have to ever deal with. Except for when it matters, and then it’s good to know you’re covered in the system as best you can be.

It took me until today to get around to increasing my UIM and BI limits w/ Geico. To increase UIM and BI limits to 500/500k was $14/month, 1/1 million is $20/month.

Geico said their PIP maxes out at 15k, but you can buy an additional 10k medical coverage for ~8/year. But, if you have good health insurance that would go into play after the 15k PIP, so that’s the better option if you have it.

I’d note that I have both car and motorcycle insurance. The moto insurance is cheaper for my older, 250cc motorcycle. That might be a good option for the cheapest/easiest way for non-motor vehicle owners to get coverage as needed. Until there’s a better option/solution…

Eric,

Glad you found this post helpful.

In my experience, motorcycle coverage does not include PIP as part of the standard coverage package and it is my understanding that insurance sellers don’t have to include it or point out its absence to customers unless specifically asked.